1st Quarter, 2026

The headwinds are economic and the crosswinds geopolitical.

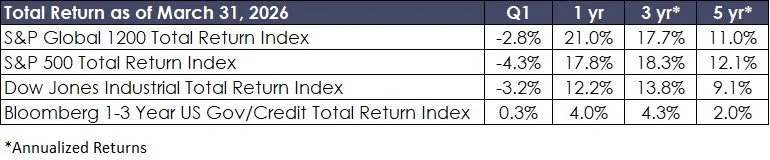

The Markets

The investment landscape shifted abruptly at the end of February as conflict involving the United States, Israel, Iran, and Lebanon escalated into a major regional confrontation. Markets were forced to absorb a geopolitical shock of unusual significance, and with it, a sharp repricing of energy, inflation expectations, and risk.

The most immediate consequence has been a meaningful energy shock. While the global economy is less energy-intensive than it was in prior decades, energy remains deeply embedded in transportation, manufacturing, agriculture, and consumer prices more broadly. As a result, investors are now confronting an uncomfortable combination: a renewed inflation impulse arriving just as growth expectations were already moderating. Near-term inflation expectations have moved higher, even as longer-term inflation expectations have thus far remained relatively more anchored.

This has created a difficult market environment. Known headwinds—including elevated valuations in select areas, persistent fiscal deficits, and structurally higher long-term borrowing costs—are now being complicated by an unpredictable geopolitical conflict. In such periods, financial markets tend to move quickly to discount fear, and the pressure to react can become intense.

We would caution against overreaction. In our experience, environments like this often lead investors to pursue complex or expensive hedging strategies in situations where no perfect hedge exists. Complexity and leverage rarely improve outcomes when uncertainty is already elevated.

The Economy

At the start of 2026, expectations for U.S. economic growth were already modest and had been drifting lower since late 2025. The principal drag has been the cumulative burden of still-elevated living costs, which has weighed on both household confidence and spending capacity.

One of the more important features of the current economy has been the uneven source of consumer resilience. Spending has held up better than many expected, but much of that support has come from the rising wealth effect enjoyed by higher-income households rather than from broad-based gains across the full consumer base. That dynamic can persist for a time, but it also introduces fragility. If asset values come under sustained pressure, consumer spending may weaken more quickly than headline data currently suggest.

At the same time, the gravitational pull of public sector deficits continues to intensify. Federal borrowing needs were already substantial, and the added fiscal burden associated with a prolonged Gulf conflict is unlikely to ease pressure on long-term interest rates. In practical terms, this remains a different interest rate environment than the one investors became accustomed to over much of the prior decade.

The recent Pakistani-brokered pause in U.S.-Iran hostilities is a constructive development insofar as it may provide a path toward negotiation. However, it does not yet appear to resolve the broader strategic tensions involving Israel, Iran, and Lebanon. That distinction matters, and until it becomes clearer, economic and market uncertainty are likely to remain elevated.

Observations of the Gulf War

The conflict has now extended well beyond its initial phase and increasingly bears the characteristics of a broader regional war of attrition.

At the outset, the objectives appeared comparatively defined: degrading Iran’s nuclear capabilities and potentially reshaping the regional balance of power. Over time, however, those objectives have become less clearly bounded. Markets are not simply troubled by uncertainty; they are most unsettled when uncertainty becomes both economically meaningful and difficult to define.

Iran appears to be pursuing a strategy of endurance rather than haste—prioritizing regime continuity and internal control over a longer time horizon. That raises the possibility of a conflict that proves more persistent than initially assumed, even if intermittent pauses or partial de-escalations emerge along the way.

For investors, the practical implication is straightforward: this may not resolve neatly or quickly. Volatility, therefore, should not be viewed as a temporary anomaly, but as a rational market response to an uncertain and potentially extended geopolitical backdrop.

Investment Strategy

At IIM, our central objective remains unchanged: to preserve and grow the real purchasing power of our clients’ capital over time.

That objective becomes especially important in periods such as this, when inflation risk, geopolitical instability, and higher financing costs are all reasserting themselves at once. In our view, the most valuable discipline during unsettled periods is not prediction—it is perspective.

Our advice remains simple: be patient and stand fast.

Periods of regional disorder are unsettling, but they also tend to create opportunity. Conflicts eventually pass, even when their path is unclear, and free-market economies have historically demonstrated a remarkable capacity for resilience, adaptation, and renewal. Our task is not to predict every turn in the geopolitical landscape, but to position capital thoughtfully through it.

That means continuing to emphasize sound asset allocation, durable businesses, valuation discipline, and liquidity. It also means resisting the temptation to chase narrow “war trades” or pursue costly tactical protection at the expense of long-term compounding.

Importantly, we entered mindful of the importance of liquidity, and the flexibility it affords. Cash reserves are not only a source of stability—they are also a source of opportunity. We expect to use accumulated liquidity selectively to purchase businesses and securities that we believe represent attractive long-term value at current or potentially lower prices.

At the same time, prudence remains essential. We continue to recommend that clients earmark the cash reserves they may need for special spending requirements, distributions, or other anticipated needs over the coming year. Capital intended for long-term compounding should remain invested with a long-term horizon; near-term obligations should not depend on favorable market timing.

Our responsibility is to help clients navigate change without losing sight of enduring principles. The present environment is unsettled, but our commitment to thoughtful stewardship, disciplined risk management, and long-term value creation remains unchanged.